Market Wrap: 28/04/2017

(19:00)

NSE-NF (May): 9331 (-26

points; -0.27%)

NSE-BNF (May): 22370

(+76 points; +0.34%)

For 02/05/2017:

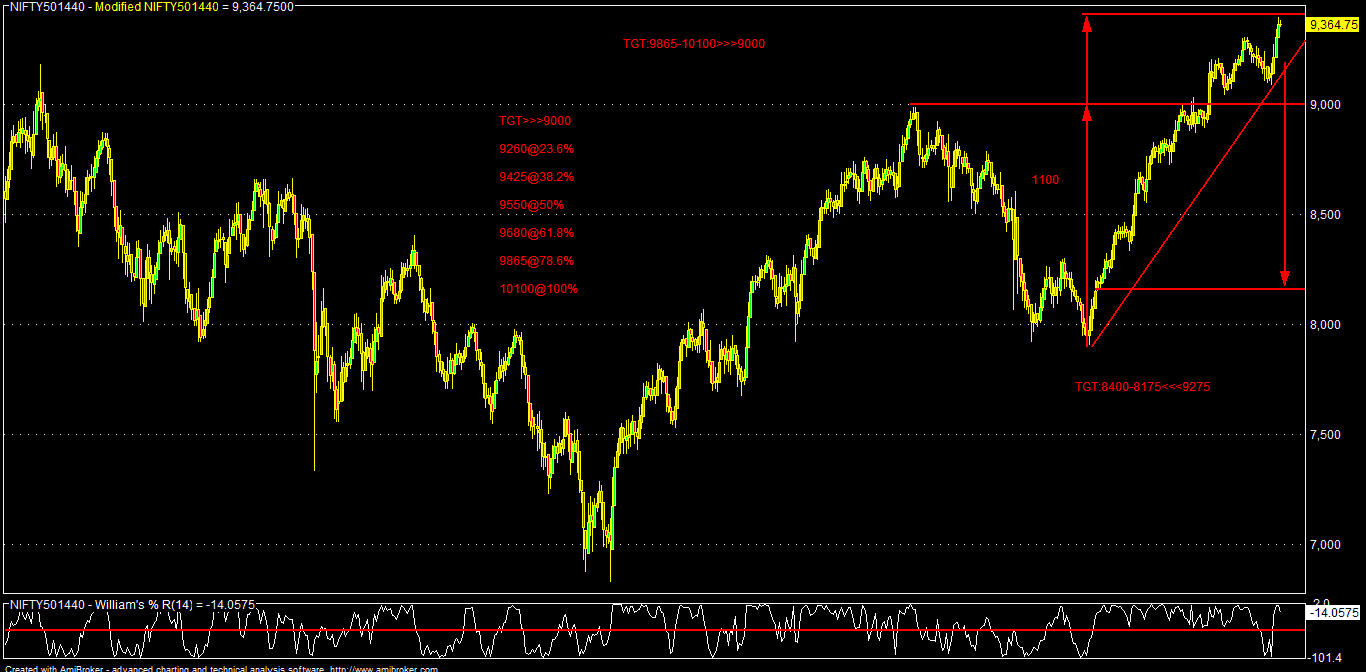

Key support for NF: 9305-9225

Key resistance for NF: 9425-9505

Key support for BNF: 22200-22100

Key resistance for BNF:

22450-22525

Time & Price action suggests that,

Nifty Fut (May) has to sustain over 9425 area for further rally towards 9475-9505

& 9550-9600 in the short term (under bullish case scenario).

On flip side, sustaining below 9405-9385

area, NF may fall towards 9305-9270 & 9225-9175 area in the short term

(under bear case scenario).

Similarly, BNF has to sustain over

22450 area for further rally towards 22525-22675 & 22800-23000 area in the

near term (under bullish case scenario).

On the flip side, sustaining below

22400 area, BNF may fall towards 22200-22100 & 22000-21700 area in the near

term (under bear case scenario).

Nifty

Fut (May) today closed around 9331, down by 0.27% in a day of consolidation

after making an opening session high of 9359 & day low of 9313. Indian

market today opened almost flat following tepid global cues amid mixed US

economic data & corporate earnings and renewed concern over NK geopolitical

issues following some of Trump’s aggressive comments. Also, Trump’s trade

protection rhetoric for SK in exchange of the “Thaad” missile defence system,

which US is installing there to counter any threat from NK have deteriorated

the Asian market sentiment today. But, in the EU session, better than expected

EU CPI at 1.9% & an upbeat core CPI at 1.2% (estimate: 1%; prior: 0.8%) has

made the global market sentiment strong and thus Indian market also followed

the suit by closing almost flat in a day of consolidation & some long

winding after the recent rally ahead of the long weekend.

An upbeat

core CPI for EU is good news for Draghi, who lamented just yesterday about

tepid pace of inflation and thus pledged to continue or even add some extra QQE

in the coming months. Thus, if today’s upward trajectory of core inflation is

continued for next few months, Draghi may be compelled to think about some

hawkish steps (rate tightening) in order to stay ahead of the inflation curve.

A depreciated currency (EUR) and a higher energy/oil prices may be primarily

responsible for the higher inflation in EU.

Meanwhile,

US have just flashed its Q1 GDP and it came terrible, though not at all unexpected

by some analysts. Q1 US GDP came as 0.7% (QOQ-Preliminary) against estimate of

1.2% (prior: 2.1%); real consumer spending also flashed poor at 0.3% against

estimate of 0.9% (prior: 3.5%). But GDP price index came as upbeat at 2.2%

(QOQ) against estimate of 2% (prior: 2.1%). Thus, the better than expected GDP

deflator (price index) may be indicating an upbeat inflation and thus despite

poor GDP headline data & tepid consumer spending, USD is gaining strength

across the board for the time being and reflation / risk trade is on. FFR is

now showing 57% probability of another two rate hikes by Fed this year against

52% prior to the GDP data. All eyes may be now on the US politics in the

weekend for the Govt shut down probability (although very low) and “war of

words” between US & NK & 100 days of Trump at the WH. But, overall a

0.7% Q1 GDP data (preliminary) may also be not good for Trump’s first 100 days

at WH, where as US GDP growth was around 1.5% on an average under Obama; this

poor GDP coupled with high probable fiscal deficits because of Trump’s tax

reform plan may not be good for the US economy and Fed may be also in the

sideline for rest of the 2017; reflation trade may also be on the dock.

Back

to home, Indian market (Nifty) today gyrated in a narrow range in absence of

any meaningful domestic cues. So far Q4 report cards are mixed; but some of the

PSBS has reported quite upbeat numbers with some improvement in the NPA resolution

front. Market is also expecting some consolidation among the PSBS after some

meaningful resolution of the stressed assets issues & an effective NPA

resolution policy by the Govt/RBI. Thus Bank Nifty is trading very strong,

although valuation may be quite stretched.

Today

Govt indicated that it will recapitalize the PSBS by the remaining Rs.10000 cr

of the Indradhanush plan by three tranches. Also Govt is working on a plan for takeover

of stressed assets by the PSBS; i.e. role of an ARC itself (?) and

consolidation of the PSBS to 4-6 large entities only. These are all helping the

PSBS; but we have to also keep in mind that being a financial year end (March’17),

traditionally Q4 is always a better quarter for NPA recoveries. This year, DeMo

in Q3 may have also helped the banks to prune some of its NPA as many borrowers

had repaid in old DeMo notes. Thus, market may look forward further in Q1 &

Q2FY18 for the actual NPA resolution trend.

Today

IMF predicted that India’s GDP may accelerate towards 8% in the mid-term on the

back of GST implementation along with UID based targeted subsidy distribution.

But, IMF also cautioned about India’s bad loan (NPA), stressed corporate balance

sheet and lack of labour reforms.

Although,

GST is still now scheduled to be implemented from July’17, it may be delayed to

Sep’17 or even to April’18 due to lack of preparations and clarity about rate

structures and issues about input tax credit (ITC) Incidentally, Govt may be also

thinking actively to change the Indian FY system from March-April to Jan-Dec in

keeping with trends for most of the global economies. Thus, if Govt go ahead to

change the FY system this year, then GST may be also implemented from Jan’18

instead of July/Sep’17. But this ongoing confusion about actual implementation

date may be also causing uncertainties among the traders

(retailers/distributors) and also the manufacturers as they are hesitant to

stock or produce heavily, keeping in mind the ITC issues. Thus GST disruption

may also affect the H1FY18 earnings of the street to some extent and we may see

again some earning expectation adjustment (downgrade) in the middle of the

year.

SGX-NF

BNF