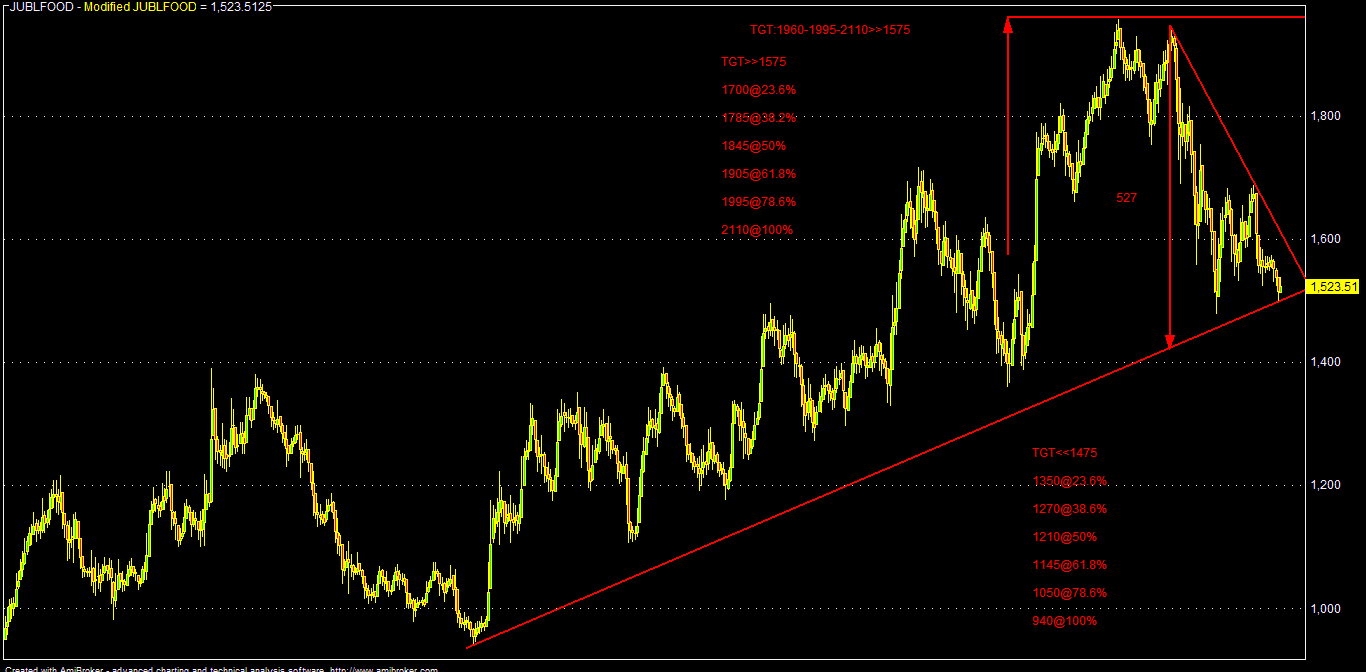

1500-1475 Might Be Very Good Demand Zone For JFL

CMP: 1519

Buy: 1500-1475

TGT: 1588-1615 & 1645-1690 (1-3M)

TGT:1737-1775-1857-1960-1995 & 2110 (12-24M)

TSL<1440

Note: Consecutive closing below 1440 for any reason, JFL can fall up to to 1415-1385-1360 & 1265-1230 zone, where investors can again accumulate for better buying average.

Some key takeaways & Rationale:

As par reports, JFL's global competitor, Yum's (KFC/Pizza Hut/Taco Bell) sales has declined nearly 9% in India due to sharp decline in SSSG (Same stores sales growth) in Q2 (-18%).

The scrip (Yum) crashed 18% in one day after it published its quarterly result on 6-th Oct in US as it missed wall street expectations quite significantly. Sluggish growth in SSSG for China market for the slowdown there may be the biggest concern for Yum, as nearly 50% of its OPM comes from China.

Expected SSSG for Yum in China was 9.6%, while it came around 2% !!

Yum's concern was also reflected in JFL scrip and analysts are also apprehending some negative effect in SSSG for JFL in the Q2FY16. Market is expecting a consensus SSSG of around 6% in Q2 for JFL.

There was also another concern because of CCD IPO in the same QSR (Quick service restaurant) segment. Although retail participation was tepid, there was heavy HNI applications for anchor portion and some funds may be flowing from JFL portfolios to CCD as par market buzz. Also there will be another similar but bigger IPO from Starbucks which is launching shortly.

As par analysts, in QSR industry, both JFL & Yum are sizeble players and JFL's long term performance is significantly better than Yum. For the last three quarters SSSG for JFL has moved into positive territory while the same for Yum India's worsened from -11% to -18%.

While there may be low base effect for JFL, the declining SSSG for Yum may be translating into higher sales growth & customer shifting preference for JFL. Many analysts are projecting long term SSSG for JFL at around 10-12% !!

JFL has good pricing power & innovations in menu too and that coupled with lower input/raw material costs and sequentially higher SSSG may result in substantial improvement in projected EPS and the stock price.

JFL has gross & net operating margin of around 75% and 12.5%. Due to better operating leverages. recovery in SSSG and expected contributions from Dunkin Donuts, net margin may improve by around 2.5% over the next two years.

SSSG is very important factor in QSR (like GRM in oil & gas industry). As par analysts at GS, even an average 2% positive change in SSSG, there may be 6-10% EPS improvement in FY-17-18 and 14% change in TP of 1958/- per share in JFL.

Downside risk to this SSSG is limited/lower price increase in the near term and sudden change in consumer's quick food preference.

Analysts at BOA-ML is also expecting JFL's SSSG at 6.5% in Q2FY16 followed by improvement in margin due to better operating leverage and sets a TP of 2100/- for the stock.

Analysts are also pointing out that over the last few years, Yum brands are consistently loosing market share to JFL (Domino's Pizza) as the later have actually improved its market share from 55% to almost 72% currently. Also Yum has some issues with their franchises.

Analysts are expecting an average 22% top line growth in Q2FY16 for JFL on the basis of management's positive commentary about SSSG and its favorable base effect (-5% YOY).

Analysts at Nomura are also concerned about the slow recovery in urban consumption, intense competition in QSR space and they are doubtful about the projected SSSG and sets a TP of 1282/- from an earlier TP of 1120/- for JFL (i.e. "bears" are also upgrading the stock to some extent).

Thus various ratings on the stock are translating an average TP of 1700/- for JFL by FY-16.

The stock was already corrected by around 25% in Sep from its early July peak against the broader market correction of around 12%. Although it has given positive return of more than 100% in the last two years against 78% in Nifty in the same period (approx:5120-9120).

No doubt, JFL is an expensive stock going by any valuation metrics. But its high PE is justifiable by its aggressive store/franchise expansions, improved discretionary spending by favorable Indian demographics, strong balance sheet having zero debt and excellent cash flow, superb management and controls over input cost. JFL has now more than 1000 stores all over India and more than 30% of its sales are coming from "online" mode, which is very cost effective for acquiring & servicing clients.

JFL is much ahead of others, like Yum/Mac etc in QSR primarily for its wide distribution network and aggressive expansion of stores. While some competitors are closing stores, JFL is rapidly opening more to virtually every important nook & corner of the country. India is now world's 2-nd largest Domino's Pizza market after US, surpassing even UK !!.

JFL always enjoyed a "scarcity premium" in the QSR market, because of its aggressive expansion of stores as competitors were lagged behind.

Another thing is that "value for price" conscious Indian middle class consumers will always favour a packet of Pizzas in lieu of a cup of roasted coffee available almost at the same price. They will rather enjoy a hot coffee for 20/- in lieu of spending 200/- for the same effect.

Technically, JFL has strong support in the 1500-1475 zone and sustaining above 1575-1690, it may scale 1960-2110 in the days ahead (FY:16-17).

Looking ahead, Market will concentrate into the actual result & management's guidance scheduled to be released on 6-th Nov for JFL. Also Q3 & part of Q4, being the festival season in India, we can expect sequentially better sales & bottom line in the next two quarters.

In India, QSR has great potential for growth, if there is some regulatory changes in the form of giving permissions for at least some kind of limited "Express Bear" along with regular menus. In that scenario, we may find it quite difficult to found an empty seat in the physical stores, which are now almost vacant to the extent of 50%, even in the weekends.

In any way, due to increase in discretionary spending for the last few years, weekend "Pizza Party" is almost a ritual in every middle class Indian family, specially if there is a kid in the family.

Going forward, we can see this trend to be sequentially higher due to overall expected economic recovery, rapid urbanization etc.

As par BG metrics & current market parameters:

Present median valuation of JFL may be around: 1400 (FY:15/TTM EPS)

Projected fair valuations might be around: 1650-1995-2135 (FY:16-18/Projected EPS)

| SCRIP |

EPS(TTM) |

BV(Act) |

P/E(AVG) |

Low |

High |

Median |

200-DEMA |

10-DEMA |

| JUBLFOOD |

19.07 |

102.13 |

65 |

1413.34 |

1386.40 |

1399.87 |

1611.49 |

1550.65 |

| JUBLFOOD |

26.25 |

72.05 |

65 |

1658.19 |

1626.59 |

1642.39 |

1611.49 |

1550.65 |

| JUBLFOOD |

38.5 |

93.25 |

65 |

2008.17 |

1969.90 |

1989.04 |

1611.49 |

1550.65 |

| JUBLFOOD |

44.3 |

120.75 |

65 |

2154.13 |

2113.08 |

2133.60 |

1611.49 |

1550.65 |

Analytical Charts: